By the end of 2024, the Medicare Part D coverage gap-commonly called the donut hole-will disappear for good. But until January 1, 2025, millions of seniors are still stuck in a confusing, expensive phase where they pay more out of pocket for prescriptions. If you’re taking regular medications and your total drug spending hits $5,030 in 2024, you enter the donut hole. That’s not a rumor. It’s the current rule. And if you don’t know how to manage it, you could end up paying hundreds or even thousands more than you should.

What the Donut Hole Actually Means in 2024

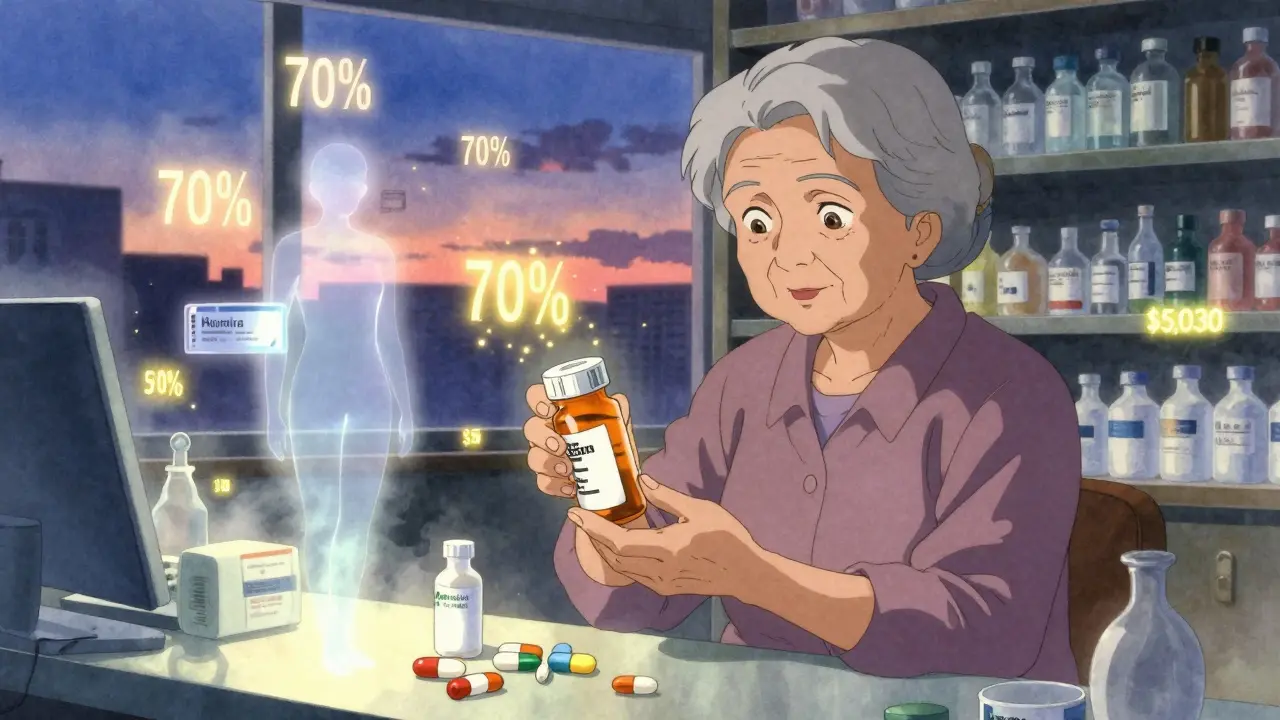

The donut hole isn’t a loophole. It’s a phase in your Medicare Part D plan where your insurance stops paying most of your drug costs. You’ve already paid your deductible (up to $590 in 2025), and your plan covered drugs up to $5,030 in total drug costs (including what you paid and what your plan paid). Now, you’re on your own-sort of.Here’s the catch: you still pay 25% of the cost for both brand-name and generic drugs. But that’s only part of the story. For brand-name drugs, the manufacturer gives you a 70% discount. That discount counts toward getting you out of the donut hole. For generics, there’s no manufacturer discount. So if you’re on Humira, Enbrel, or Repatha, you’re getting help from the drugmaker. If you’re on metformin or lisinopril, you’re not.

This means two people on the same plan, taking different drugs, can have wildly different out-of-pocket costs. One person might spend $3,300 to get out of the gap. Another might spend $6,000. That’s not a typo. That’s how the math works.

Why This Matters More Than You Think

In 2022, nearly 1 in 5 Medicare Part D enrollees hit the donut hole. That’s over 10 million people. And according to the Medicare Rights Center, 68% of those people said they changed how they took their meds because of cost. Some skipped doses. Others split pills. One Reddit user, a Medicare counselor with 12 years of experience, shared a story about a client paying $1,200 a month for Humira during the gap-forcing them to choose between medicine and groceries.It’s not just about cash. It’s about health. Skipping insulin? Not an option. Skipping blood pressure meds? That leads to ER visits, hospital stays, and higher costs down the road. The Medicare Payment Advisory Commission found that eliminating the donut hole could reduce prescription abandonment by 18-22%, saving the system $1.2 billion a year in avoided care.

How to Slash Your Costs Before the Donut Hole Ends

You don’t have to wait for 2025 to save money. Here’s what actually works right now.- Check your drug’s tier. Your plan puts drugs into tiers. Tier 1 is cheapest. Tier 3 or 4? That’s where the donut hole hits hardest. If your drug is on Tier 3, you’re paying 25% coinsurance until you hit $5,030. Ask your pharmacist or log into your plan’s website. If your drug is on a higher tier, ask your doctor if a lower-tier alternative exists.

- Switch to generics. If you’re on a brand-name drug like Eliquis or Lyrica, ask if a generic is available. GoodRx found that switching to generics can save $1,200 to $2,500 a year. For example, switching from brand-name Adderall to generic amphetamine salts can cut your monthly cost from $200 to under $30.

- Use manufacturer assistance programs. Big drug companies have patient programs. Amgen’s program for Repatha cut one user’s cost from $560 to $5 a month during the gap. AbbVie helps with Humira. Merck helps with Januvia. Go to the drugmaker’s website and search for “patient assistance.” You’ll need your prescription and income info. Many are free.

- Get 90-day supplies. Mail-order pharmacies often charge less for 90-day fills. Medicare.gov says you can save 15-25% on copays. If you take a drug daily, this is an easy win. Some plans even waive the deductible for mail-order orders.

- Apply for Extra Help. If your income is under $21,870 (single) or $29,580 (married), you qualify for the Low-Income Subsidy. It covers your deductible, lowers your copays, and eliminates the donut hole entirely. In 2023, 12.6 million people got it. You might be one of them and not know it.

Use the Medicare Plan Finder-Now

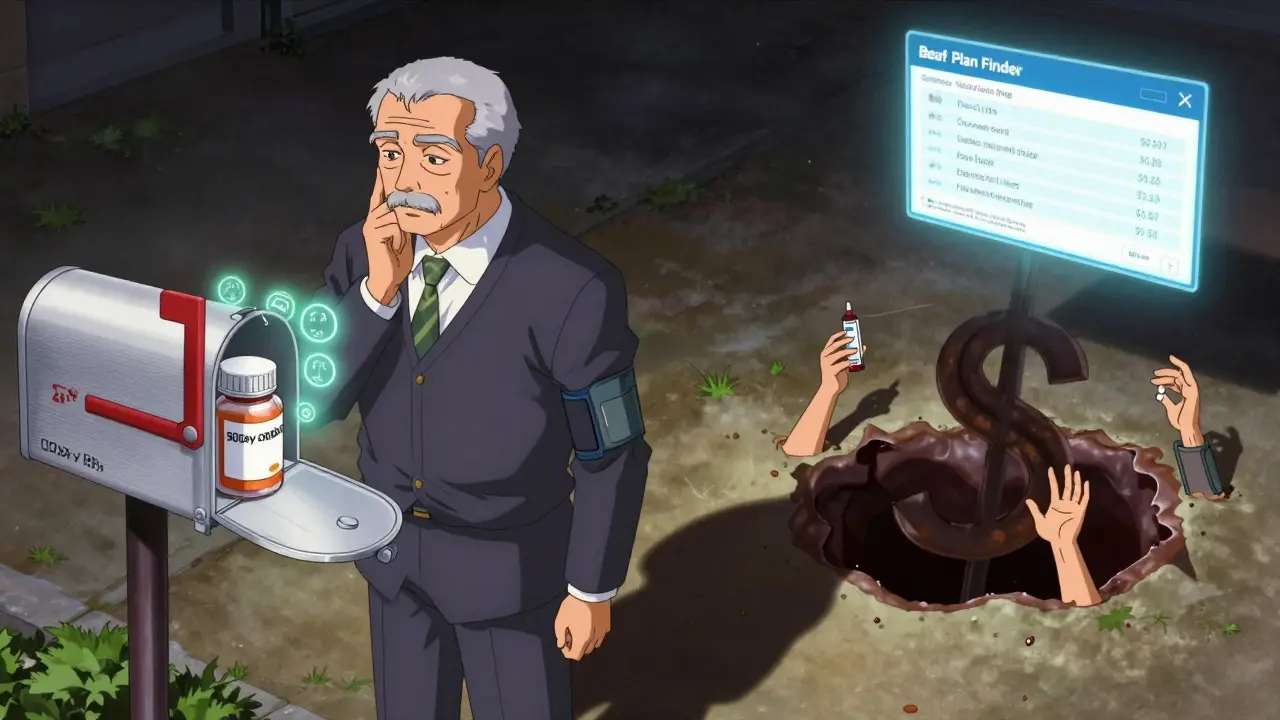

Your plan changes every year. Just because you stayed with the same one last year doesn’t mean it’s still the best. The Medicare Plan Finder tool lets you type in your exact drugs and see how much each plan will cost you in 2024. The National Council on Aging found that people who use this tool save an average of $1,047 a year.Don’t just pick the cheapest premium. Pick the plan that’s cheapest for your meds. A plan with a $30 monthly premium might charge $150 for your insulin. Another with a $60 premium might charge $25. That’s a $1,500 difference over the year.

Spread Out Your Purchases (Carefully)

If you’re close to hitting the $5,030 threshold, you can delay entering the donut hole by spreading your fills across different pharmacies. Buy your first 30-day supply at CVS, the next at Walgreens, the next at your local independent pharmacy. This spreads your spending across multiple pharmacies, so you don’t hit the cap as early.But be careful. This only works if your plan tracks all your spending across pharmacies. Most do now. If you’re unsure, call your plan. Don’t risk getting hit with a surprise bill because you thought you were avoiding the gap.

What’s Changing in 2025 (And Why You Should Care)

Starting January 1, 2025, the donut hole is gone. Forever. You’ll pay no more than $2,000 out of pocket for all your Part D drugs in a year. After that, your plan covers everything. No more 25% coinsurance. No more manufacturer discounts counting toward your cap. No more confusion.But there’s a twist. The $2,000 cap is only for what you pay. It doesn’t include what your plan pays or what manufacturers pay. So if you’re on a $1,000-a-month drug, your plan might still pay $500 of it. That’s fine. You only care about your out-of-pocket.

Experts warn that premiums might rise slightly for some people-especially lower-income beneficiaries who used to benefit from manufacturer discounts counting toward catastrophic coverage. But for most, the change is a win. The average annual savings for those who hit the gap in 2022 is estimated at $980. That’s like getting a free prescription every few months.

What to Do Right Now

You have less than a month before the donut hole disappears. Here’s your checklist:- Log into your Medicare account and check your 2024 drug spending. Go to Medicare.gov and use the Plan Finder.

- Call your pharmacist. Ask: “Am I close to the $5,030 threshold?”

- Check if your drugs have generics or lower-cost alternatives.

- Visit the manufacturer’s website for your drugs. Look for “patient assistance” or “copay card.”

- Apply for Extra Help if your income is under $21,870 (single) or $29,580 (married).

- Review your 2025 Annual Notice of Change. It arrived in September. Don’t ignore it.

The donut hole was designed as a cost-control tool. But it became a trap for seniors. The fix is coming. But until then, you don’t have to suffer. You have tools. You have options. Use them.

What is the Medicare Part D donut hole in 2024?

The donut hole is the coverage gap in Medicare Part D that starts after you and your plan have spent $5,030 on covered drugs in 2024. Once you enter this phase, you pay 25% of the cost for both brand-name and generic drugs. Manufacturer discounts on brand-name drugs count toward getting you out of the gap, but there are no discounts for generics.

Do I still pay full price in the donut hole?

No. You pay 25% of the total drug cost for both brand-name and generic medications. For brand-name drugs, the manufacturer pays 70%, and your plan pays 5%. For generics, your plan pays 75% and you pay 25%. The 70% manufacturer discount counts toward your out-of-pocket total to help you exit the gap faster.

How do I know if I’m in the donut hole?

Your plan sends you a notice when you enter the coverage gap. You can also track your spending using the Medicare Plan Finder on Medicare.gov. Look for your total drug costs, which include what you paid, what your plan paid, and manufacturer discounts on brand-name drugs. When that total reaches $5,030 in 2024, you’ve entered the donut hole.

Can I avoid the donut hole by switching plans?

You can’t avoid it entirely, but you can delay entering it or reduce how much you pay while in it. By switching to a plan with lower copays for your specific drugs, you can stretch your spending further. Using the Medicare Plan Finder to compare plans based on your exact medications can save you over $1,000 a year and help you stay out of the gap longer.

What happens after January 1, 2025?

The donut hole is eliminated. Starting in 2025, you’ll pay no more than $2,000 out of pocket for all your Medicare Part D drugs in a year. After that, your plan covers 100% of your drug costs. This change is part of the Inflation Reduction Act and applies to everyone enrolled in Medicare Part D.

Are there programs to help if I can’t afford my meds?

Yes. Many drug manufacturers offer patient assistance programs that can reduce your cost to $0-$10 a month. You can also apply for Extra Help (Low-Income Subsidy) if your income is below $21,870 (single) or $29,580 (married). This program covers your deductible, lowers your copays, and eliminates the donut hole. Thirty-seven states also have Medicare Savings Programs that help with premiums and out-of-pocket costs.

Should I wait until 2025 to fix my drug costs?

No. The changes in 2025 are helpful, but you’re still in the donut hole now. Waiting means paying more this year. Use manufacturer discounts, switch to generics, apply for Extra Help, and use mail-order pharmacies to cut costs now. The $2,000 cap won’t help you if you’re already spending $5,000 out of pocket in 2024.

Mike Rengifo

December 17, 2025 AT 12:36Man, I just hit the donut hole last month on my insulin. Paid $400 for a 30-day supply. My buddy told me about the manufacturer coupon-turned out I qualified for $0 copay. Should’ve checked sooner. Don’t be like me.

Ashley Bliss

December 18, 2025 AT 01:41This system is a moral failure. People are choosing between feeding their families and staying alive. And the pharmaceutical companies? They’re laughing all the way to the bank while seniors split pills like it’s some kind of DIY survival challenge. This isn’t healthcare-it’s a blood sport dressed in blue and white.

Meenakshi Jaiswal

December 18, 2025 AT 02:08If you’re on Humira or Enbrel, go straight to the manufacturer’s website and apply for their patient assistance program. I helped my mom get it last year-her cost dropped from $1,100/month to $10. It takes 2-3 weeks, but it’s worth it. Also, call your pharmacy and ask if they have a discount card-some have better deals than your plan.

Andrew Kelly

December 19, 2025 AT 12:47Let’s be honest-this whole ‘donut hole’ was engineered by bureaucrats who think seniors are too dumb to understand co-pays. The real issue? Medicare’s contract with Big Pharma. They’re getting kickbacks disguised as ‘manufacturer discounts.’ That’s why generics get screwed. Wake up, people. This isn’t about cost-it’s about control.

Anna Sedervay

December 19, 2025 AT 23:37One must acknowledge the structural inequities embedded within the Medicare Part D framework, particularly the perverse incentive structure that privileges brand-name pharmaceuticals through federally-sanctioned rebate mechanisms. The fact that generics receive no manufacturer subsidy is not an oversight-it is a deliberate policy failure rooted in the commodification of human health. One wonders whether the architects of this system have ever personally experienced the visceral terror of skipping a dose of antihypertensive medication.

Dev Sawner

December 20, 2025 AT 04:45According to CMS 2023 data, 78% of beneficiaries who entered the coverage gap were unaware of manufacturer assistance programs. This is not a failure of policy-it is a failure of education. The government must mandate that pharmacies display eligibility information at point-of-sale. Furthermore, the $2,000 cap in 2025 will disproportionately benefit high-cost drug users while leaving moderate users with unchanged premiums. The math does not lie.

shivam seo

December 20, 2025 AT 19:08Why are we even talking about this? In Australia, we just pay $7 per script. No donut holes. No coupons. No ‘patient assistance programs.’ Just medicine. You guys built a $4 trillion healthcare system and still can’t give people pills without a PhD in bureaucracy. Pathetic.

Mahammad Muradov

December 21, 2025 AT 16:18The author neglects to mention that the $2,000 cap in 2025 will not include the value of manufacturer discounts. This means that for those on expensive biologics, the true out-of-pocket cost may still exceed $2,000 if the plan does not fully absorb the 70% discount. The policy is misleadingly labeled as ‘eliminating the donut hole’-but it merely shifts the burden from the beneficiary to the plan sponsor. A semantic sleight of hand.